As the owner of a small business, you already understand the importance of your personal and business credit scores.

A good credit score is key for obtaining credit cards, loans, and other financing you need in order to grow your business or make large purchases in your personal life, such as buying a home or car. But many people, even those who are entrepreneurs and proprietors of their own companies, don’t know much about business credit scores, how they’re determined, and where they can check their scores.

There are several business credit bureaus that provide business credit scores, including FICO. The FICO (Fair Isaac Corporation) credit scoring company provides personal credit scores that are used by banks, credit unions, and other financial institutions when they’re considering applications for loans and credit cards.

FICO also provides businesses with a score, which is called the FICO SBSS score. However, the FICO SBSS score is different from the other major business credit scores on the market. Here’s what you need to know about your business FICO score, what’s looked at in order to score your business, and how you can strengthen your score.

What is a Business FICO Score?

The FICO Small Business Scoring Service (SBSS) is a numerical score between 0 and 300 which reflects your business’ financial state. This score serves as a valuable shortcut for investors and lenders who are considering financing a company, as it gives them an idea about the likelihood that a company will repay a loan, and whether that company is on solid financial ground. However, the FICO SBSS score is different from the other major business credit scores on the market. Business lenders use the SBSS score along with other business credit scores to make faster, more accurate lending decisions.

How Does FICO SBSS Work?

Your FICO SBSS is determined by factoring in both your business credit data and your personal credit, in order to provide potential lenders or investors with a big picture overview of your business’ overall fiscal standing. Notably, as the proprietor of a small business, FICO considers your personal financial history as intertwined with your business’ financial standing. That means that even if you have excellent business credit history, if your personal credit is spotty, that will be reflected in your FICO score.

What Does FICO Look at to Create a Business Credit History Score?

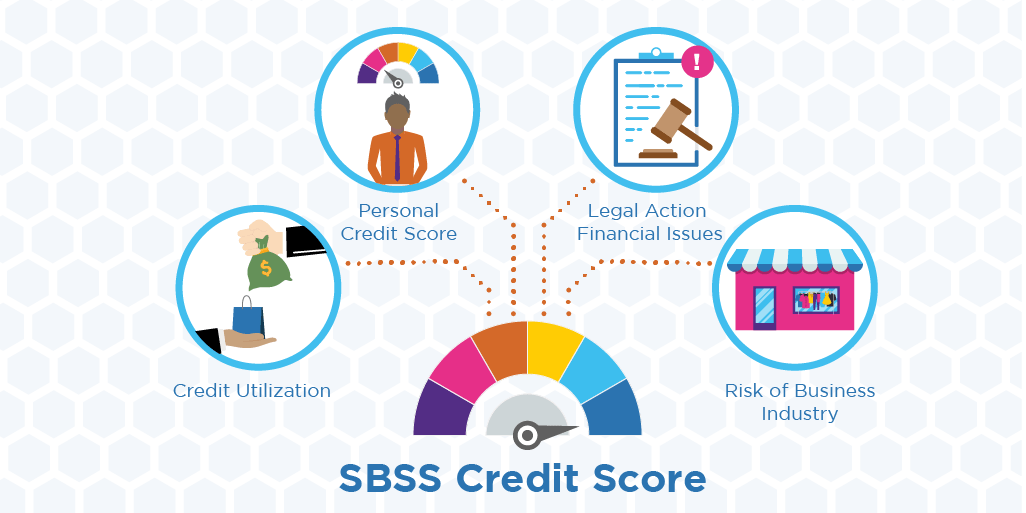

FICO takes a number of elements within from your personal and business credit history and current standing in order to determine your score, including:

Your personal credit score

Personal and business credit utilization

Legal action stemming from financial issues, such as liens or bankruptcies declared by you, your current business, and/or previous businesses

Whether you’re consistently making payments to lenders, vendors, and suppliers

The age, size, and revenue of your business

Your business’ number of employees and assets

The overall risk of your business’ industry

Notably, as a business owner of a small business, FICO considers your personal financial history as intertwined with your business’ financial standing.

After pulling both your personal credit report and business credit report, FICO then assigns you a numerical score that serves as an indication of your business’ financial stability and fiscal track record.

About the FICO SBSS Score Range

The FICO SBSS system is relatively straightforward. Based on your credit history and the various factors considered by FICO, your business is given a number between 0 and 300. The higher your score, the better – the closer to 300 you land, the more likely it is that lenders will consider your business to be creditworthy and low risk.

Can a Poor SBSS Credit Score Hurt my Business?

Unfortunately, yes. A score lower than 140 essentially makes your business unable to get a small business loan from either government agencies and private lenders. A low score serves as a red flag to warn lenders that there’s a significant risk that you won’t pay back your loan, should they finance you.

More than 7,000 business financing lenders, including the American government’s SBA (Small Business Administration), will require a minimum score of at least 160 or higher in order to lend to your business. While the SBA will occasionally make exceptions for businesses with a score of 140, in all likelihood, you’ll need at least 160 – and preferably higher – to score an SBA loan. Many private lenders require 180 as a minimum starting point, but some are willing to accommodate a score as low as 160 – and that will likely come along with less favorable terms for you, such as an overall lower amount funding, shorter amount of time in which to repay it, higher interest rates, and more upfront collateral. Essentially, if you want to be able to obtain financing with advantageous APRs, flexibility in terms of the time period for loan repayment, and lower or even no collateral requirements at all, you must have a stellar FICO business score.

What are the Best Ways to Improve my FICO SBSS Score?

The good news is that there are steps small businesses can take today to help boost their FICO SBSS score.

Focus on Your Personal Credit

Because your personal credit history is a significant contributor to your FICO SBSS score, you should ensure that your personal score is as high as possible. That means making sure to make payments on your personal loans and credit cards on time each month and address any debts or disputes you have as quickly as possible. Utilizing your credit responsibly – meaning that you avoid maxing out your cards each month, and have some credit available leftover at the end of the billing period – will also improve your personal credit score.

Reevaluate Your Business’ Financial Practices

Are you putting large purchases on your business credit card, then struggling to make payments on time, or can only cover part of the balance? What about using every last bit of credit you have – whether on a business credit card or from your business line of credit – on a regular basis? Or are you obtaining inventory from suppliers, then finding yourself unable to pay their invoices? If any of the above apply to you, it’s time to take a hard look at your business’ financial practices and adopt a more sustainable approach towards your money.

You need to be sure that you can pay all your bills on time, every time, and that you’re not dependent on maximizing your credit constantly in order to cover your expenses. Once you establish and implement a solid financial strategy for your company and personal finances that sees you gain more control over your spending and expenses, your FICO SBSS will steadily improve over time. While it won’t skyrocket over the night, you should reap the benefits of your new financial practices within several months of changing the way you spend and save.